Under the R&D Tax Incentive, a distinction has to be made between core and supporting R&D activities and these need to be reported separately to AusIndustry. To claim the R&D Tax Incentive, you must undertake at least one core R&D activity.

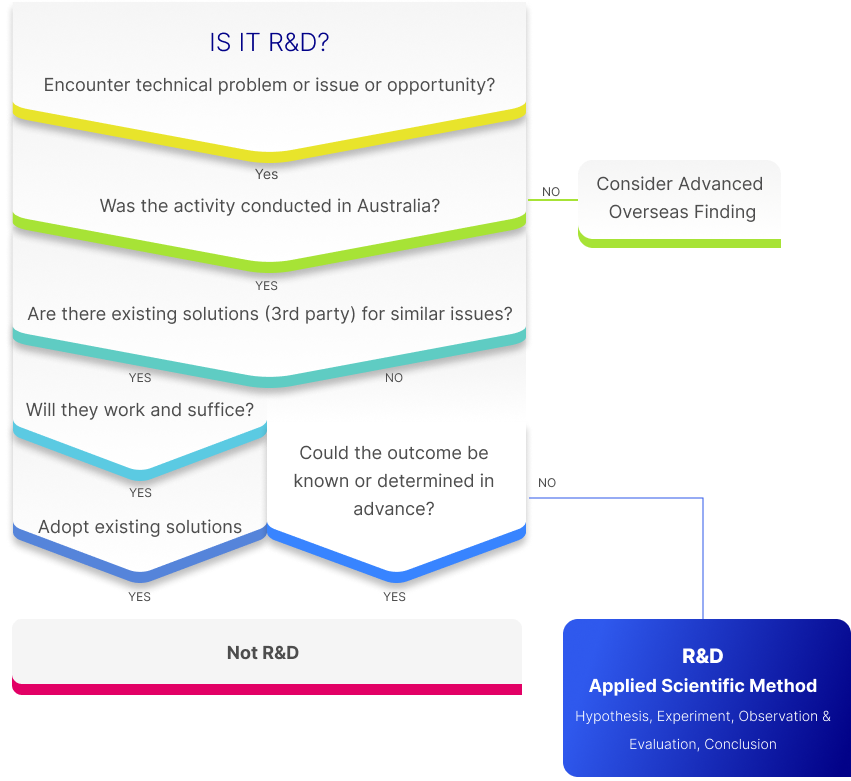

Use this flow chart to determine if your business activities are eligible.

Definition of core activities

Core R&D activities are experimental activities:

1. Whose outcome cannot be known or determined in advance on the basis of current knowledge, information or experience, but can only be determined by applying a systematic progression of work that:

– Is based on principles of established science; and

– Proceeds from hypothesis to experiment, observation and evaluation, and leads to logical conclusions; and

2. That are conducted for the purpose of acquiring new knowledge (including knowledge or information concerning the creation of new or improved materials, products, devices, processes or services).

Further to this general principle, there are some activities that are specifically excluded from qualifying as core R&D activities.

Definition of supporting R&D activities

Supporting R&D activities are activities directly related to core R&D activities. If supporting activities are undertaken for normal operational reasons, they only remain eligible where the dominant purpose for conducting them is to support core R&D activities.